1️⃣Investment idea of the week

2️⃣Charts of the Week

As ususal this week , the market has been defined by the news from the Iran conflict and by the rapid shift from optimism to renewed caution.

Early in the week, sentiment improved on the back of reports pointing to a de-escalation between the United States and Iran, with expectations of smoother conditions in the Strait of Hormuz. Markets responded accordingly: oil prices eased, equities stabilized, and volatility declined, reflecting a temporary reduction in perceived tail risk.

However, in the last 24 hours, that narrative has partially reversed. Fresh tensions and disruptions in maritime traffic have reintroduced uncertainty, pushing oil higher again and leading to a more defensive positioning across assets. 🌍

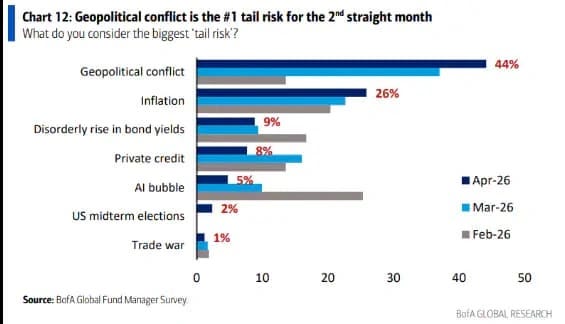

This evolution directly reflects the message in Chart 12, where according with BofA the geopolitical conflict and Hormuz situation is a clearly illustrated by this dynamic: sentiment can shift within hours based on geopolitical headlines, highlighting the fragility beneath otherwise stable market conditions. 🛢️

On the other hand, Chart 14 adds depth by identifying where a systemic shock could emerge, with US shadow banking seen as the main source at 57%. This distinction is crucial. Geopolitics explains short-term volatility, but the real structural vulnerability lies within credit markets, particularly in less transparent segments such as private credit.

The link between both charts is therefore straightforward: geopolitical events act as catalysts, while financial fragility determines the scale of the impact. A sustained shock, for example through higher energy prices or tighter liquidity, could quickly transmit into stress across leveraged structures. 🏦

Finally, and at the same time, secondary concerns such as AI-related capital expenditure and consumer credit suggest that investors remain attentive to how leverage and capital allocation are evolving, so we have here a multiple risks which are interconnected and capable of reinforcing each other. 📉

3️⃣Articles of the Week

More articles from other creators which are interesting for this week!

Mr Deep-Value | @mrdeepvalue

Kaneshita Construction

Asset-heavy business mispriced as declining: Market treats it like a low-growth, commoditized construction company, but underlying value sits in stable cash flows, tangible assets, and conservative balance sheet → disconnect between perceived cyclicality and actual resilience.

Re-rating depends on capital allocation, not growth: Thesis is not expansion but unlocking value (dividends, buybacks, efficiency); without this, it risks staying a “cheap forever” stock despite solid fundamentals and downside protection.

Quality Value Investor | @qualityvalueinvestor

Greens Co

Mispriced asset-light transition: Shift toward franchise/mixed model improves margins and capital efficiency, but market still values it like a low-quality, asset-heavy operator.

Tourism leverage with execution upside: Earnings tied to inbound demand recovery, but real upside comes from pricing power, network expansion, and disciplined capital allocation rather than just cyclical tailwinds.

I hope you find the content useful.😀

May the investment be with you.

Magno Investments Research

⚠️ DISCLAIMER | LEGAL ADVICE⚠️

Magno investments is not an entity authorised or supervised by any financial authority and does not provide investment services or regulated financial advice.

All material provided (articles, presentations, theses, ideas, opinions and analyses) are for informational and educational purposes only and does not constitute a recommendation to buy, sell or hold financial instruments, nor does it constitute personalised advice

Magno Investments Research are not responsible for the use made of this information or the veracity of its sources.

Magno Investments and/or its writer and contributors may hold, directly or indirectly, positions in the securities mentioned in the content. These positions may be changed at any time without prior notice.

Before investing in a real account, it is necessary to have the appropriate training or otherwise delegate this task to a professional duly authorized to do it. Magno Investments is not responsible for the use that members make of the information or for any losses arising from their investments.