1️⃣Investment idea of the week

We’ve just finished our UK Ideas Week, here’s the full market research.

Market Research UK

As part of our ongoing series analysing small-cap markets across different countries, this time we turn our focus to the United Kingdom.

Now we’re kicking off Switzerland Ideas Week, a market known for quality, resilience and world-class businesses.

2️⃣Charts of the Week

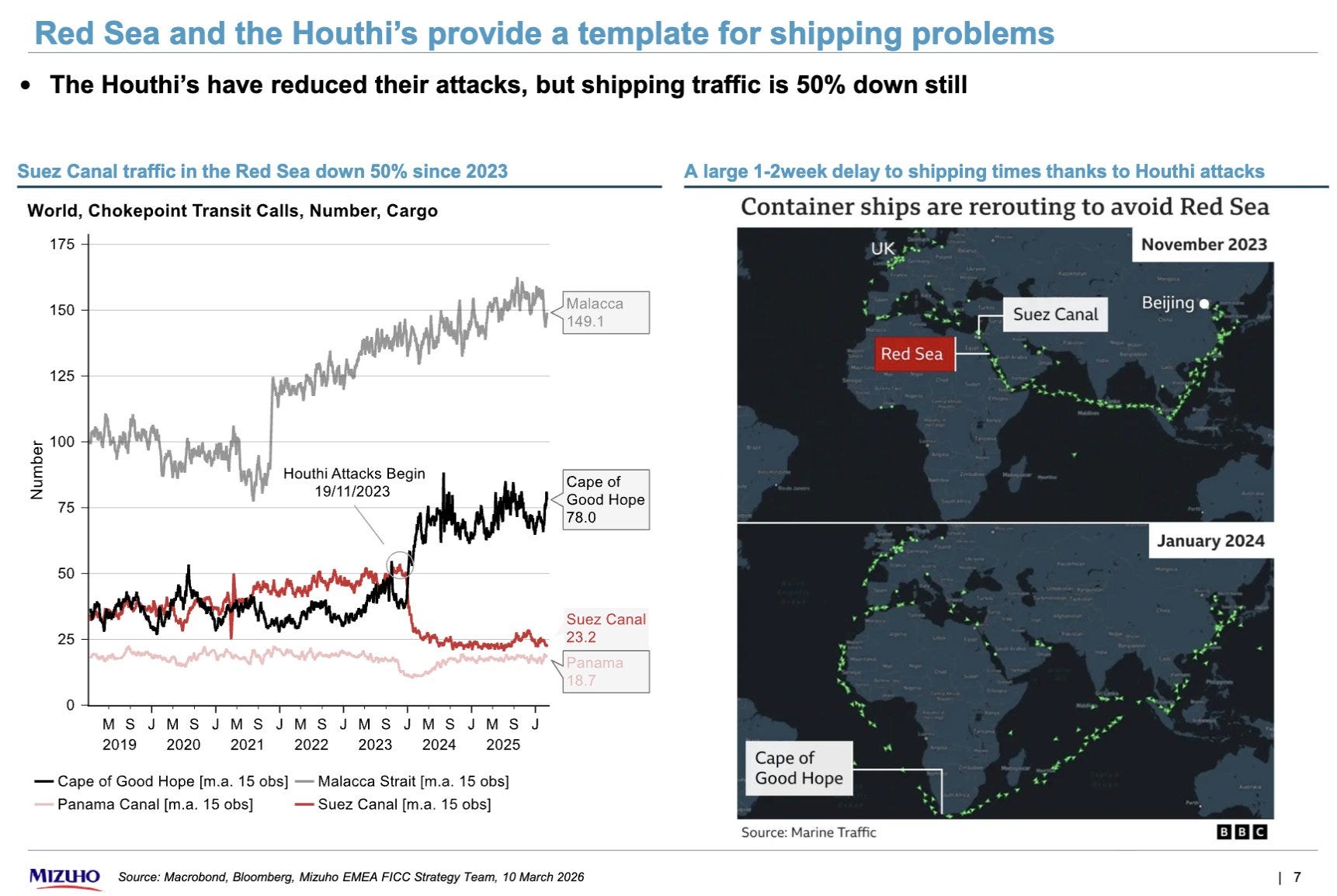

The week starts with shipping disruption. Despite fewer attacks, Red Sea traffic remains ~50% below normal, with vessels still rerouting via the Cape of Good Hope. This signals a shift from a temporary shock to a structural supply chain issue, reinforcing the idea that the conflict is becoming prolonged and entrenched, with no near-term resolution in sight. 🚢⚠️

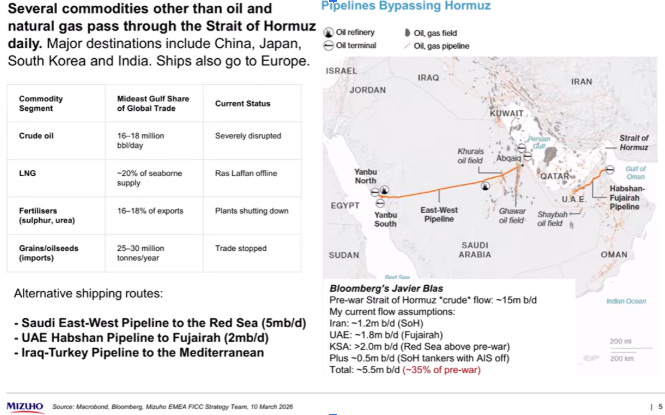

From there, the story moves to Hormuz, which is where the real energy risk sits. A very large share of oil, LNG and other key commodity flows still depends on that corridor, and the alternative pipelines shown in the slide help, but they do not fully replace normal seaborne volumes.

That is the key market point. The issue is not just whether some cargo can still move, but whether the system can keep moving at the scale and speed the market needs. If disruption drags on, the next step is not just delays, but tighter physical supply, scarcity in some segments and eventually demand destruction. 🛢️🌍

On top of that, the latest attacks on refining and processing infrastructure add a second layer of pressure. The image of the smoke and the summary table make the point clearly. Damage to these assets is not just about a short lived fire headline, it can mean real capacity loss and long repair timelines. In the case shown, the estimated impact is around 17 to 20% of capacity, with a possible recovery window of 3 to 5 years. That tells you the market is now dealing with more than transport disruption. It is also dealing with the risk of lost processing capacity, which makes the whole supply chain even less flexible. 🔥🏭

That is why Brent is not the whole story. The more relevant signal is what happens to the actual regional crude benchmarks, especially Dubai, Oman and related Middle East barrels that price the oil Asia really buys. And that is where stress is showing up more clearly.

So even if governments talk about protecting shipping lanes or releasing strategic reserves, the market still sees a system under pressure. Put simply, flows are less reliable, infrastructure is taking damage, and physical tightness is building faster than policy reassurance can calm it. 📈⛽

Articles of the Week

This week we bring you, as always, several interesting creators.

Giles Capital | @gilescapital

• Market backdrop & opportunity set: explains how geopolitical tensions (oil spike, Hormuz disruption) are driving volatility and fear, creating pockets of mispricing where patient capital can find opportunities

• Core idea generation approach: curates multiple deep value ideas globally (e.g. low P/E, high FCF yield, asset undervaluation) showing a systematic process of finding mispriced companies with strong fundamentals and insider alignmen

The Value Philosopher | @valuephilosopher

• Why he sold Spotify: explains how the thesis played out and the market fully recognised the business, with margins improving and valuation no longer offering clear upside

• Core investing lesson: buying mispricing and selling once normalisation occurs, stressing patience, discipline and capital reallocation once the easy returns are captured

⚠️ DISCLAIMER | LEGAL ADVICE⚠️

Magno investments is not an entity authorised or supervised by any financial authority and does not provide investment services or regulated financial advice.

All material provided (articles, presentations, theses, ideas, opinions and analyses) are for informational and educational purposes only and does not constitute a recommendation to buy, sell or hold financial instruments, nor does it constitute personalised advice

Magno Investments Research are not responsible for the use made of this information or the veracity of its sources.

Magno Investments and/or its writer and contributors may hold, directly or indirectly, positions in the securities mentioned in the content. These positions may be changed at any time without prior notice.

Before investing in a real account, it is necessary to have the appropriate training or otherwise delegate this task to a professional duly authorized to do it. Magno Investments is not responsible for the use that members make of the information or for any losses arising from their investments.