1️⃣Investment idea of the week

2️⃣Charts of the Week

Markets started the week on edge after the escalation of the Iran conflict, which directly threatens global energy and trade routes. Around 20% of global oil shipments pass through the Strait of Hormuz, making any disruption there critical for both energy markets and global supply chains. Investors are now watching closely whether the conflict becomes prolonged, as this would keep pressure on inflation and central bank policy. 🌍🛢️

Source: U.S. Energy Information Administration (EIA), visualization by Anadolu Agency.

The immediate reaction has been in energy and shipping costs. Oil surged close to $90 per barrel, driven by fears of supply disruption and reduced production across Gulf exporters. At the same time, shipping routes and maritime insurance costs have spiked, with some insurers withdrawing coverage in the region and freight prices on certain routes doubling in a matter of days.

This creates a second inflation channel beyond energy: logistics and global trade costs. 🚢📈

Source: www.drewry.co.uk

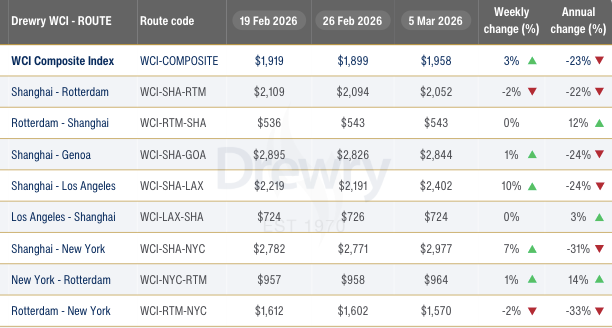

The first image (table) presents the latest data from the Drewry World Container Index (WCI), one of the main benchmarks tracking global container freight rates. The index measures the cost of shipping a 40-foot container across the world’s major trade routes. 📦💸

As of 5 March 2026, the composite index stands at $1,958 per container, with notable weekly increases on key routes such as Shanghai–Los Angeles (+10%) and Shanghai–New York (+7%).

These movements suggest that shipping markets are already starting to price in geopolitical risk, particularly as uncertainty grows around critical maritime routes and global supply chains. 🌍⚓

Source: Drewry World Container Index

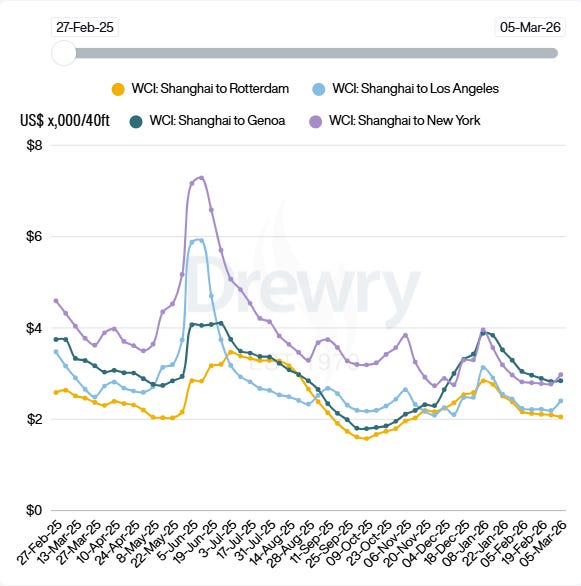

On the other hand, the second image (chart) illustrates the recent evolution of freight rates across major routes, including Shanghai–Rotterdam, Shanghai–Los Angeles, Shanghai–Genoa, and Shanghai–New York.

The chart shows how freight costs surged during the global supply-chain crisis before gradually normalizing as logistics conditions stabilized, however, the latest data points reveal a renewed upward turn in several routes, indicating that freight markets are once again reacting to disruptions and rising risk premiums. 📦📊

Historically, these dynamics can escalate quickly. When maritime routes face disruptions or insurers raise risk premiums, freight rates can spike within weeks as carriers reroute vessels, transit times lengthen, and shipping capacity tightens.📈💸

Taken together, both images reinforce the same macro point: the current geopolitical shock is not only an energy story. Rising logistics costs are beginning to ripple through global supply chains, creating an additional inflationary channel via international trade and transportation costs. 🌐⚠️

3️⃣Articles of the Week

Below, as usual you will find two articles I found particularly interesting and constructive.

Nikotes | @nikotes

• Software Darwinism in the AI Era: The article explains how AI is reshaping software markets, arguing that only the most essential, deeply embedded tools will survive while “good enough” software gets replaced.

• What Actually Survives: It highlights that software with strong customer lock-in, real mission-critical use cases, and constant improvement is far more likely to win in an AI-driven world.

CAESAR CAPITAL | @caesarcapital

• Alphabet Beyond Search: The article frames Alphabet as much more than Google Search, breaking down how its ecosystem across ads, cloud, YouTube and AI supports long-term growth.

• AI and Cloud as the Next Engine: It explains why AI integration and Google Cloud are key to reducing ad dependence and driving the company’s next phase of value creation.

I hope you find the content useful.😀

May the investment be with you.

Magno Investments Research

⚠️ DISCLAIMER | LEGAL ADVICE⚠️

Magno investments is not an entity authorised or supervised by any financial authority and does not provide investment services or regulated financial advice.

All material provided (articles, presentations, theses, ideas, opinions and analyses) are for informational and educational purposes only and does not constitute a recommendation to buy, sell or hold financial instruments, nor does it constitute personalised advice

Magno Investments Research are not responsible for the use made of this information or the veracity of its sources.

Magno Investments and/or its writer and contributors may hold, directly or indirectly, positions in the securities mentioned in the content. These positions may be changed at any time without prior notice.

Before investing in a real account, it is necessary to have the appropriate training or otherwise delegate this task to a professional duly authorized to do it. Magno Investments is not responsible for the use that members make of the information or for any losses arising from their investments.