Fund Overview

Polar Capital Global Insurance Fund is an Ireland-domiciled UCITS strategy launched in 1998 that invests exclusively in the global insurance sector.

Most equity portfolios are driven by macro cycles, interest rates, consumer demand or technology multiples. However, this fund is built around one structural mechanism: the growth of tangible book value per share in insurance companies.

Because of this, the fund is not positioned as a broad financial allocation. It is a pure underwriting portfolio, and that purity creates differentiation. In portfolio construction terms, it introduces exposure to a segment whose drivers are not identical to those of global equities or traditional financial stocks.

ISIN: IE00B4X2MP98

Structure: UCITS (Polar Capital Funds plc – Ireland-domiciled)

Investment Manager: Polar Capital LLP

Asset Class: Global Equity (Insurance sector focus)

Base Currency: GBP

Fund inception (Launch Date): 16 October 1998

Historical Performance

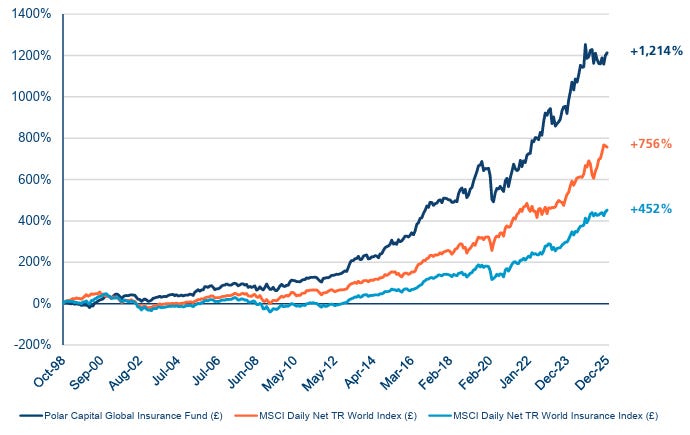

The long-term cumulative performance chart since inception is the starting point of the story.

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026 (data provided by Polar Capital & RSMR; MSCI index data for comparison).

This visual is crucial. It shows a structurally rising curve since 1998. It is not linear, and it does not avoid drawdowns. However, the key observation is the persistence of the upward trend over more than two decades. That persistence reflects something fundamental: insurance book value has compounded across multiple market regimes.

On the other hand, the annual data shows variability, which is normal. Insurance is not immune to cycles, however, what matters is that no single difficult year has broken the long-term compounding path.

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026 (Performance data provided by Polar Capital; MSCI index data for comparison).

The historical section therefore establishes two ideas: long-term compounding exists, and the return pattern is structurally distinct from broad equity sectors.

The strategy is designed to survive cycles, not avoid them. 📈⏳

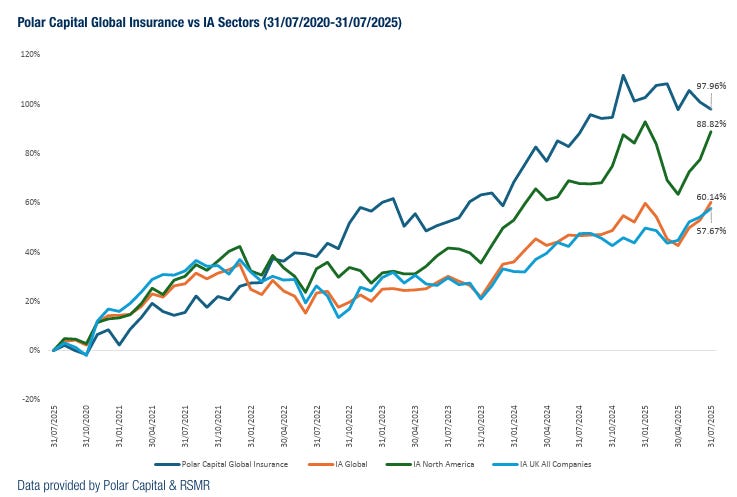

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026 (Data provided by Polar Capital & RSMR; IA sector data source: RSMR).

Accordingly with what I mentioned, I like this performance comparison between the fund’s performance pattern vs broader IA sectors. At times it leads, at times it lags, but importantly, it does not simply replicate global equity behaviour. That is the key structural value of a 100% insurance strategy. It offers potential decorrelation through different economic drivers.

Investment Philosophy

The philosophy of the fund begins with a clear conviction: risk in the world is rising, not falling. 🌍⚖️

Insurance is not discretionary consumption. It is a structural necessity embedded in the functioning of modern economies.

Accidents, natural catastrophes, cyber threats and geopolitical tensions will continue to occur. Because risk itself does not disappear, the demand for protection does not disappear either. For that reason, the fund concentrates on non-life property and casualty insurers, a segment whose demand remains resilient and far less dependent on short-term economic growth.

However, the real differentiator lies not only in demand stability, but in how insurers generate returns.

These companies assume inherently risk while maintaining conservative balance sheets. Capital is largely invested in short-duration, liquid assets so claims can be paid at any moment. In a higher interest rate environment, that liquidity is no longer idle. The shift from near-zero yields to materially higher reinvestment rates has transformed the sector’s earnings profile. What was once a low double-digit return on capital has, in many cases, moved into the mid to high teens. 📈💰

At the same time, rising catastrophe frequency has led to a broad repricing of risk. Crucially, in insurance, volatility does not automatically erode profitability. When risks increase, premiums adjust accordingly. This built-in pricing flexibility reinforces the sector’s ability to protect margins across cycles.

Ultimately, this is not a strategy reliant on predicting macro outcomes. It is grounded in the structural economics of risk transfer, underwriting discipline and capital resilience. 🏛️📘

Portfolio Snapshot

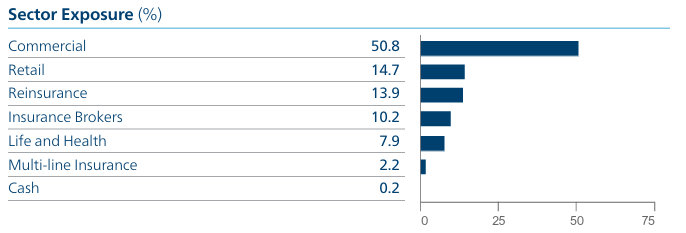

The portfolio composition reflects that philosophy directly.

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026, Portfolio Exposure (Sector Exposure % as at 30 January 2026).

Commercial insurance dominates the portfolio. Specialist commercial lines tend to reward pricing discipline, technical expertise and risk selection capability. Retail exposure is present but remains measured. Reinsurance is also included, though carefully balanced to limit excessive exposure to catastrophe volatility and earnings swings.

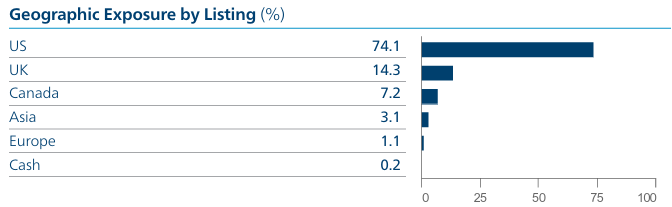

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026, Geographic Exposure by Listing (% as at 30 January 2026).

On the other hand, as you can see the United States is the deepest insurance market globally, with strong disclosure standards and developed regulatory frameworks.

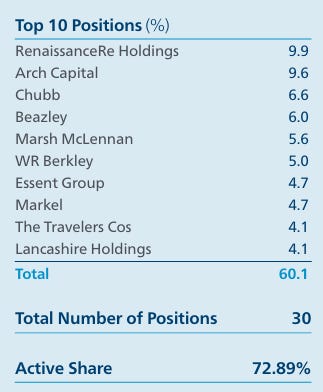

Now look at concentration and conviction.

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund (R Acc GBP), 30 January 2026, Top 10 Positions, Total Number of Positions and Active Share (as at 30 January 2026).

The top ten positions represent a significant share of the portfolio, and Active Share is high. This confirms that the strategy is genuinely active. In a specialist sector, concentration can reflect analytical edge rather than excess risk.

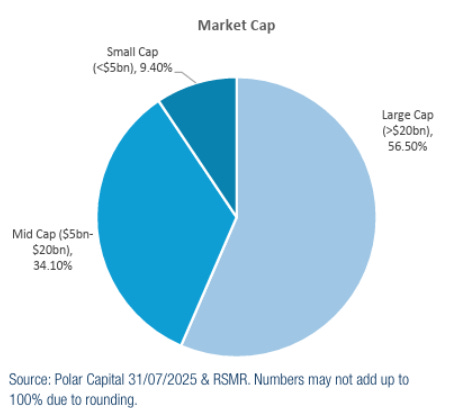

Finally, market capitalisation balance adds texture.

Source: Polar Capital LLP, Professional Investor Fact Sheet – Polar Capital Funds plc – Global Insurance Fund, 31 July 2025 (Market Cap breakdown; data provided by Polar Capital & RSMR).

With over half of the portfolio allocated to large-cap insurers, the fund anchors itself in established franchises with scale, diversified books of business and proven capital discipline. At the same time, meaningful exposure to mid-cap specialists introduces growth potential and operational agility.

This balance is deliberate. It reflects a strategy that combines stability with selective upside, rather than leaning entirely toward defensive giants or niche small-cap volatility.

In other words, the portfolio structure mirrors the philosophy: core resilience supported by targeted specialist exposure. 📊🧭

Fund Managers

The analytical depth behind the strategy is fundamental. 🧠📊

Nick Martin and Dominic Evans bring extensive experience in analysing insurance companies, a sector where small details can have major long-term consequences.

Insurance accounting can be complex, and pricing mistakes may take years to become visible. That is precisely why specialist expertise matters.

Their experience allows the fund to assess risk selection discipline, balance sheet resilience and management alignment with precision. In a sector where errors may remain hidden before surfacing suddenly, rigorous analysis becomes a structural advantage.

Why Consider Polar Capital Global Insurance

The global risk environment is becoming increasingly complex. Climate volatility, cyber threats and geopolitical fragmentation are not temporary headlines, but structural forces reshaping the demand for protection. 🌍⚡

Against this backdrop, the fund may appeal to investors seeking long-term compounding, structural diversification and exposure to a sector with disciplined capital allocation. It offers a differentiated way to participate in global equity markets through the economics of risk transfer rather than traditional macro growth drivers. 🛡️📈

To conclude, below are a couple of interviews with Nick Martin, which provide deeper insight into the fund’s investment approach and the principles that underpin portfolio construction.

⚠️ DISCLAIMER | LEGAL ADVICE⚠️

Magno investments is not an entity authorised or supervised by any financial authority and does not provide investment services or regulated financial advice.

All material provided (articles, presentations, theses, ideas, opinions and analyses) are for informational and educational purposes only and does not constitute a recommendation to buy, sell or hold financial instruments, nor does it constitute personalised advice

Magno Investments Research are not responsible for the use made of this information or the veracity of its sources.

Magno Investments and/or its writer and contributors may hold, directly or indirectly, positions in the securities mentioned in the content. These positions may be changed at any time without prior notice.

Before investing in a real account, it is necessary to have the appropriate training or otherwise delegate this task to a professional duly authorized to do it. Magno Investments is not responsible for the use that members make of the information or for any losses arising from their investments.