INVESTMENT THESIS | FUCHS SE (FPE)

Where European Industry Finds Frictionless Growth

Company Introduction

FUCHS SE is the world’s largest independent manufacturer of lubricants and related specialty products. Founded in Germany in 1931, the company has built its entire history around a single strategic focus: lubrication solutions. Unlike integrated oil majors, FUCHS deliberately chose not to engage in upstream oil extraction or fuel distribution, concentrating exclusively on developing, producing and commercializing lubricants and functional fluids for industrial and automotive applications.

Source: FUCHS SE – Investor Presentation

This focus has shaped a very specific corporate culture. Over decades, FUCHS has positioned itself not as a commodity supplier, but as a technical partner to its customers. Today, the group operates globally through more than seventy subsidiaries, serves over 100,000 customers and remains controlled by the founding family. This long-term ownership structure has reinforced a strategy centered on stability, operational excellence and capital discipline rather than short-term growth at any cost.

Sector Analysis: Industrial Lubricants Market

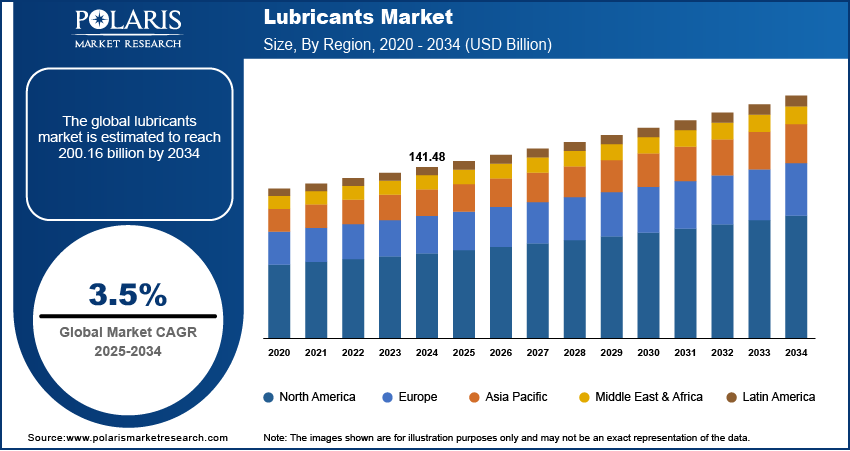

The global lubricants market is large and structurally resilient, with an estimated size that is expected to exceed $200 billion by 2034, growing at a global CAGR of approximately 3.5% over the next decade. While this headline figure may suggest a mature and slow-moving industry, it conceals a crucial distinction between low-value, volume-driven lubricants and specialty and industrial lubricants, which represent the most attractive segment of the market from an economic standpoint.

Source: Polaris Market Research – Lubricants Market Size, By Region (2020–2034)

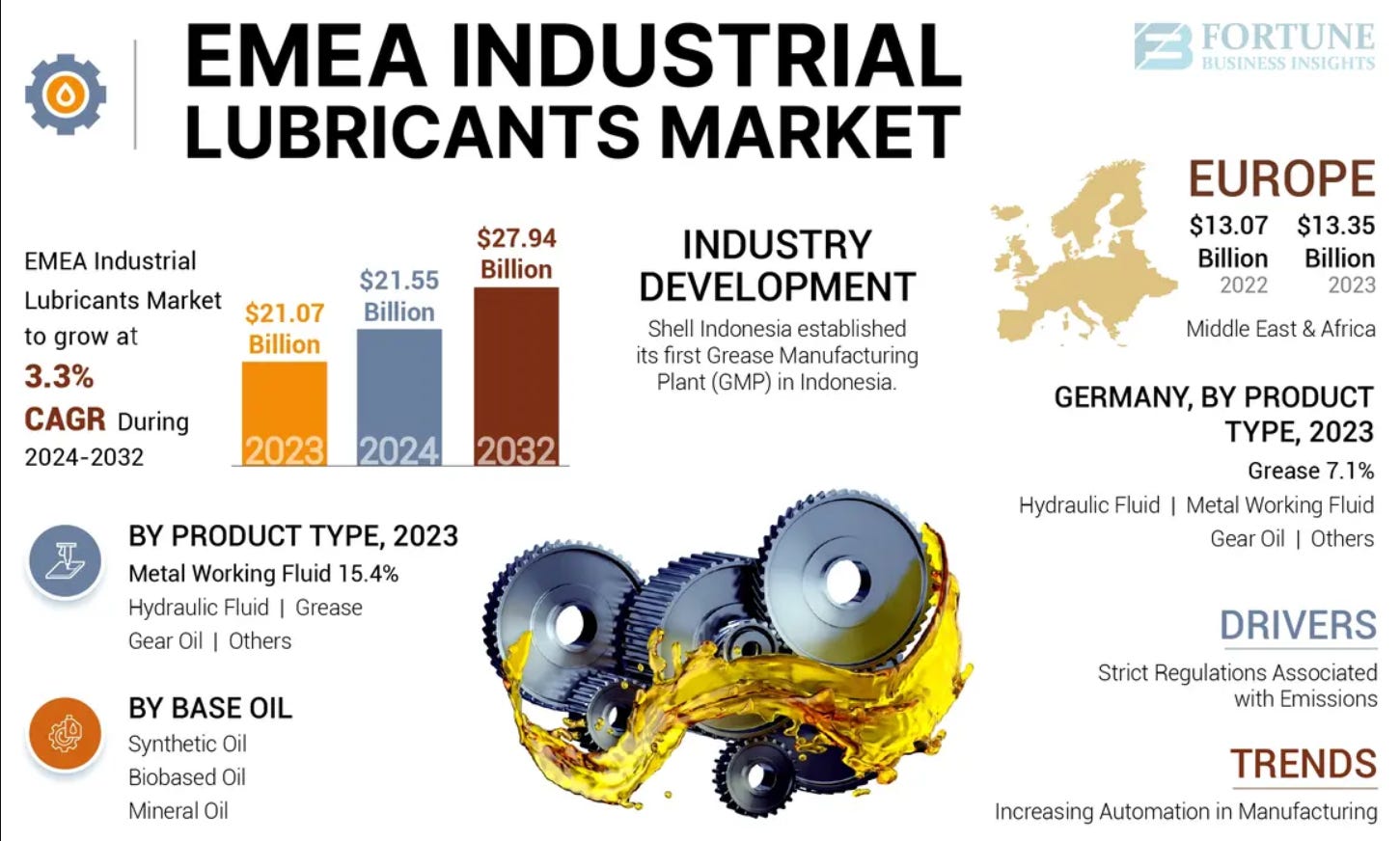

Within the EMEA region, which is particularly relevant for FUCHS, according to Polaris the industrial lubricants market is projected to grow at a CAGR of around 3.3% between 2024 and 2032, expanding from approximately $21 billion in 2023 to nearly $28 billion by 2032. Europe alone accounts for more than half of this regional market, underlining the importance of industrial activity, manufacturing density and regulatory standards in driving demand for advanced lubrication solutions.

Source: Polaris Market Research – Lubricants Market Size, By Region (2020–2034)

This growth is not primarily driven by higher lubricant volumes, but by increasing complexity and higher value per unit. As manufacturing processes become more automated and machinery more sophisticated, equipment requires lubricants that perform under tighter tolerances, higher temperatures and more demanding operating conditions. At the same time, stricter environmental and emissions regulations are accelerating the shift toward synthetic and bio-based oils, further increasing formulation complexity and value-added content.

Core Business, Segments and Geographic Footprint

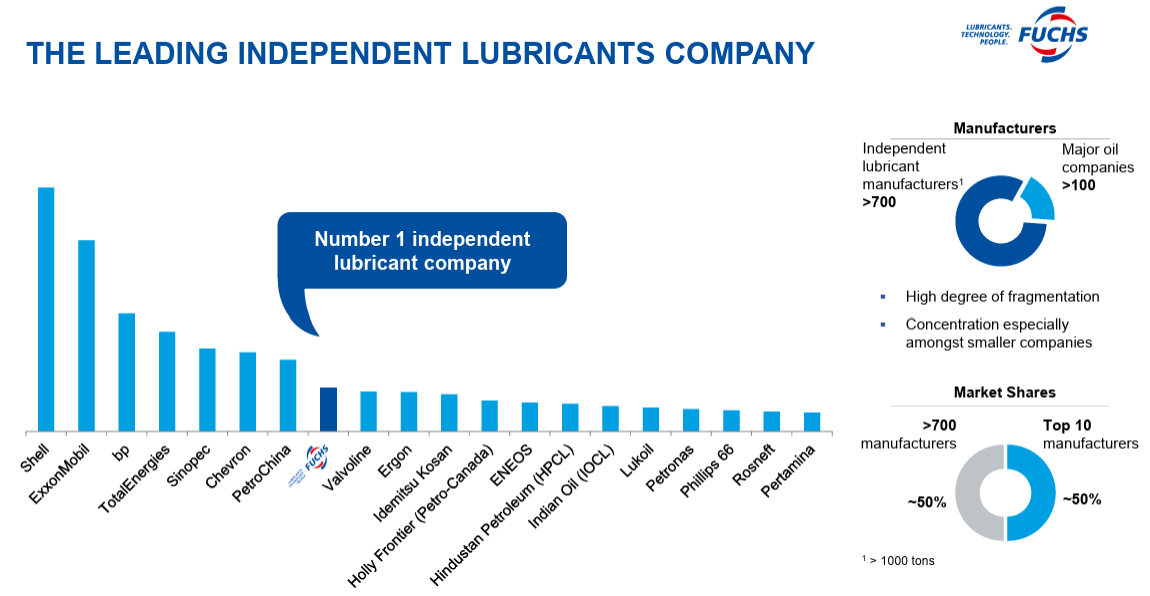

FUCHS generates revenues by developing and selling more than 10,000 lubricant formulations across industrial, automotive and specialty applications. FUCHS occupies a unique position as the world’s leading independent lubricant manufacturer in a highly fragmented global market. This allows the company to combine the focus and agility of a specialist with the scale, credibility and technical depth required to serve global industrial customers.

Source: FUCHS SE – Investor Presentation

Geographically, FUCHS operates through a highly decentralized global footprint, with more than forty production sites and over seventy operating companies worldwide. Europe remains the largest region, while Asia-Pacific and the Americas are growing steadily. This combination of local customer proximity and global R&D capabilities represents a durable competitive advantage that is difficult to replicate.

Source: FUCHS SE – Investor Presentation

Industrial lubricants exhibit a strong cost–impact asymmetry: while they represent a negligible marginal cost, failure can trigger disproportionate economic losses through downtime or equipment damage. This shifts purchasing behavior away from price and toward reliability and performance, structurally favoring specialized suppliers. As a result, the segment benefits from high switching costs, recurring demand and long product lifecycles, making it both defensive and structurally growing. FUCHS is positioned precisely in this most attractive part of the market, capturing pricing power, resilient demand and long-term customer relationships rather than relying on volatile commodity volumes.

Growth Drivers and Strategic Positioning

This highly decentralized footprint is not only a defensive advantage, but also a critical enabler of future growth. Looking forward, FUCHS is well positioned to benefit from several structural trends.

The electrification of transport increases demand for new thermal management fluids, while renewable energy infrastructure requires advanced lubrication solutions to reduce maintenance costs and extend asset life.

High-tech industries such as semiconductors and medical technology also demand increasingly sophisticated products with very high performance requirements.

Source: FUCHS SE – Investor Presentation

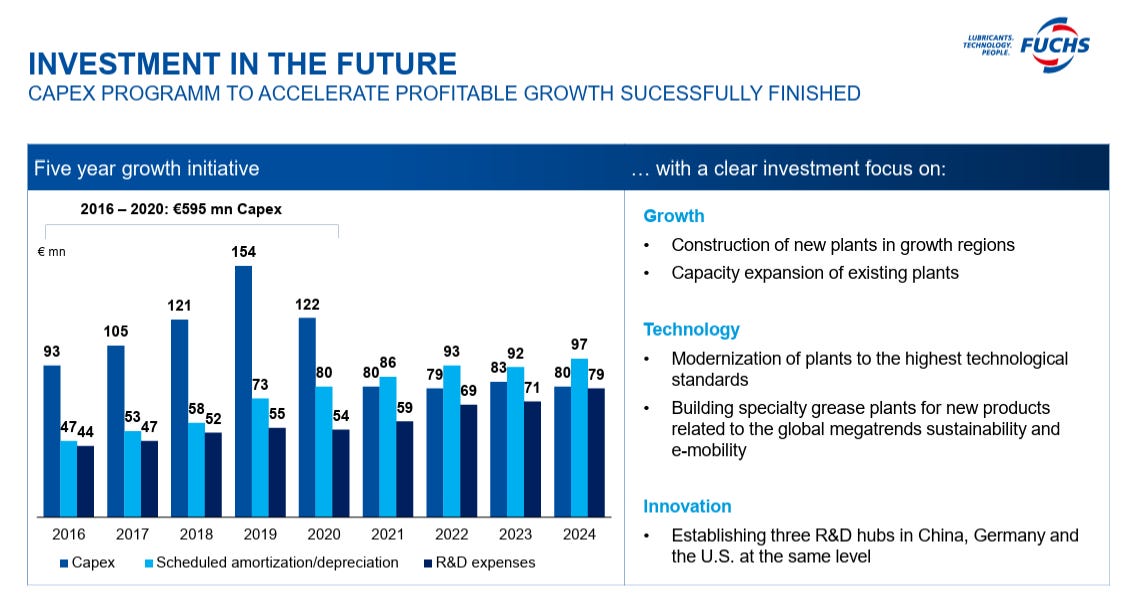

These growth drivers are reinforced by sustained investment in technology and capacity. As mentioned FUCHS has consistently allocated capital to expand production in growth regions, modernize existing plants and strengthen its global R&D network.

This ensures that innovation remains closely aligned with customer needs, while new products can be industrialized and deployed locally with speed and reliability.

Source: FUCHS SE – Investor Presentation

Key Financials and Business Quality

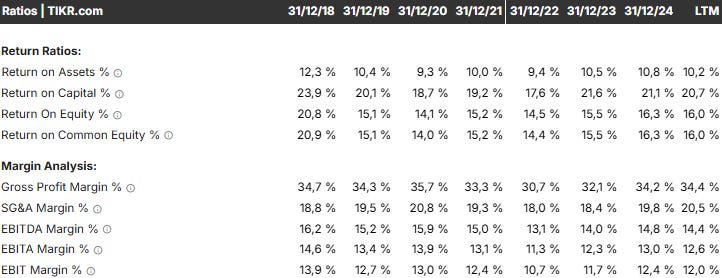

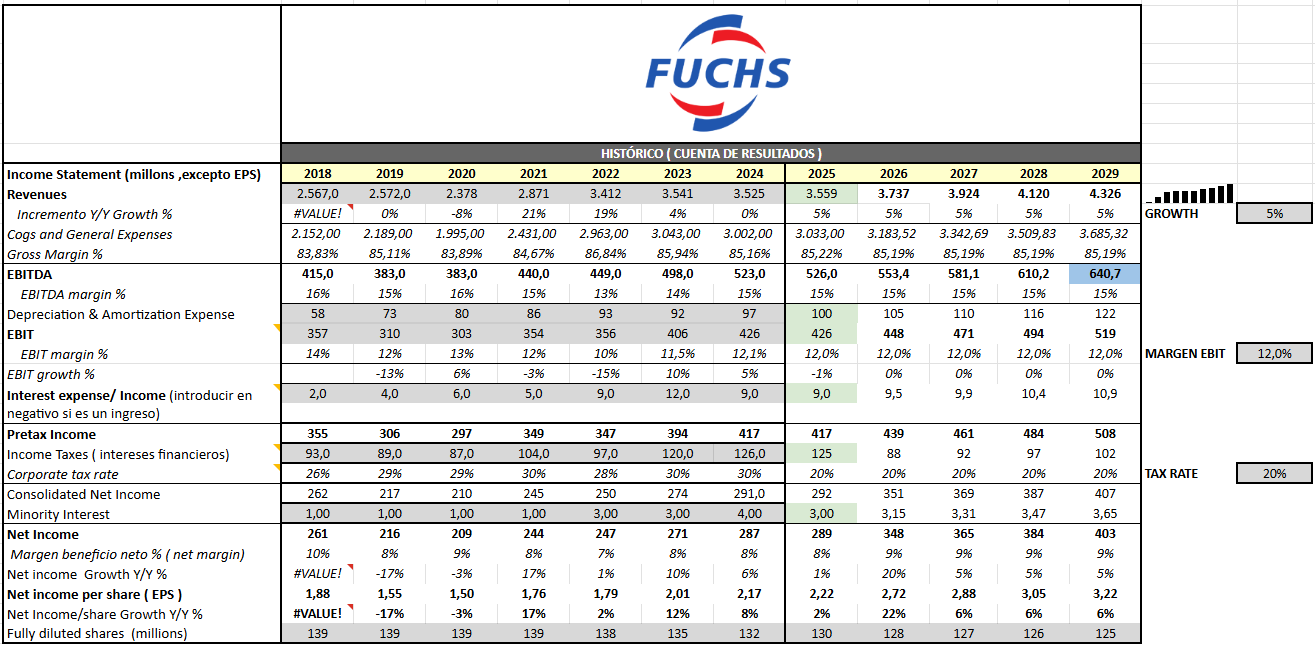

FUCHS displays financial characteristics that clearly differentiate it from a typical chemicals company. Operating margins are consistently in the low-teens, supported by gross margins above 30%, reflecting its positioning in specialty lubricants rather than commoditized products.

More importantly, the company generates a high return on invested capital, around 20% on average, indicating that growth translates into genuine economic value.

Source: TIKR.com

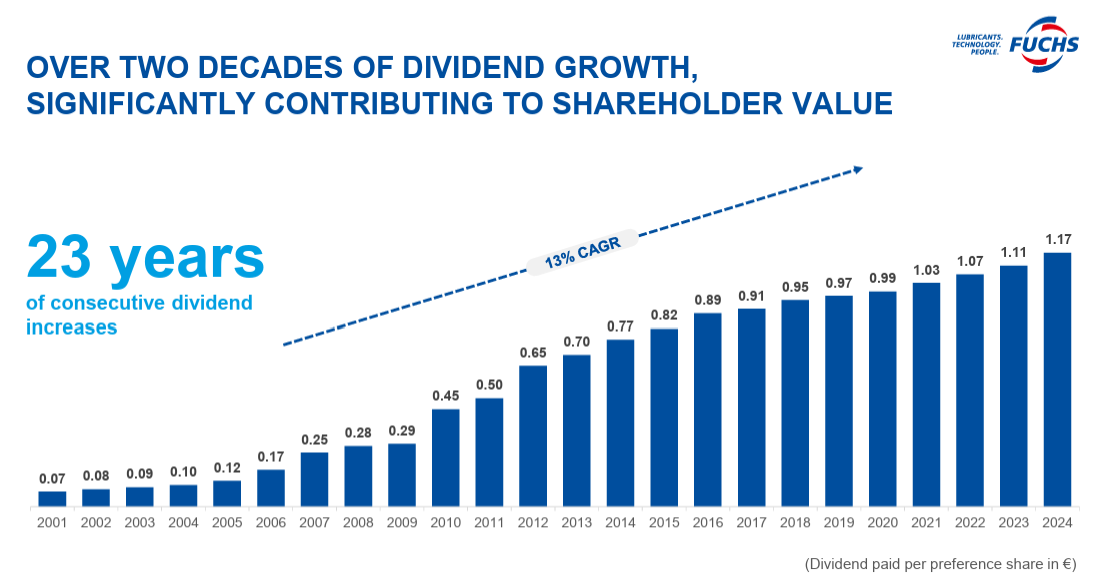

This business quality is reinforced by a long-standing shareholder return profile. FUCHS has delivered over two decades of uninterrupted dividend growth, underpinned by stable free cash flow generation and a conservative balance sheet.

Low financial leverage allows the company to fund organic growth, pursue selective acquisitions and return capital to shareholders simultaneously, without compromising financial flexibility.

Source: FUCHS SE – Investor Presentation

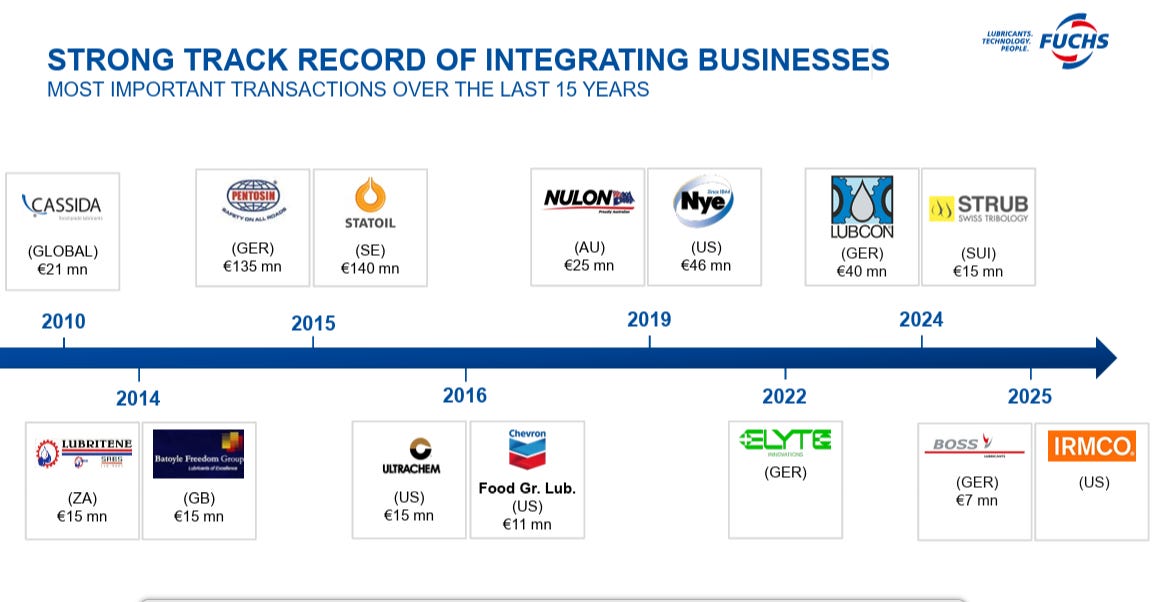

Growth has been predominantly organic, driven by volume, pricing and mix improvements, while acquisitions have played a complementary role.

Importantly, M&A has been small, targeted and focused on niche technologies or geographic strengthening, avoiding the execution and integration risks typically associated with large-scale transactions. This disciplined approach has preserved margins and returns over time.

Source: FUCHS SE – Investor Presentation

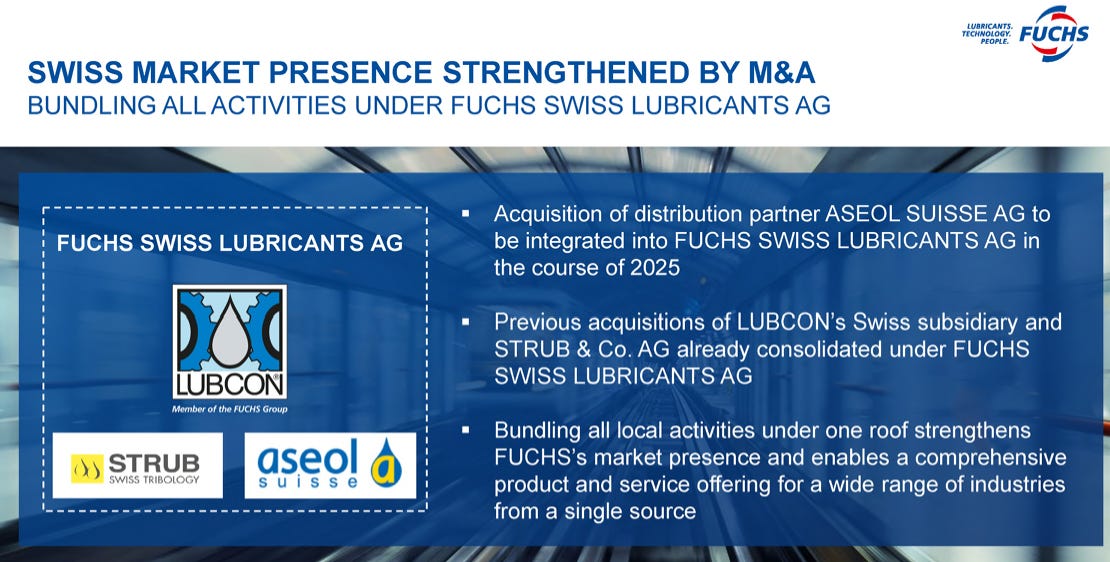

Recent transactions, such as the consolidation of activities in Switzerland, illustrate this strategy in practice. Rather than pursuing transformational deals, FUCHS uses acquisitions to bundle capabilities, strengthen local market positions and broaden its product offering, enhancing operational efficiency while remaining close to customers.

Source: FUCHS SE – Investor Presentation

The main risks facing FUCHS relate to industrial cyclicality, raw material price volatility and execution risk in acquisitions. However, the company has historically demonstrated an ability to pass through cost increases over time and to maintain profitability during economic downturns.

The focused and disciplined nature of its M&A strategy further limits integration risk, reinforcing the overall resilience of the business. Overall, the risk profile is mitigated by the essential nature of the products, the high level of customer integration and the conservative financial structure

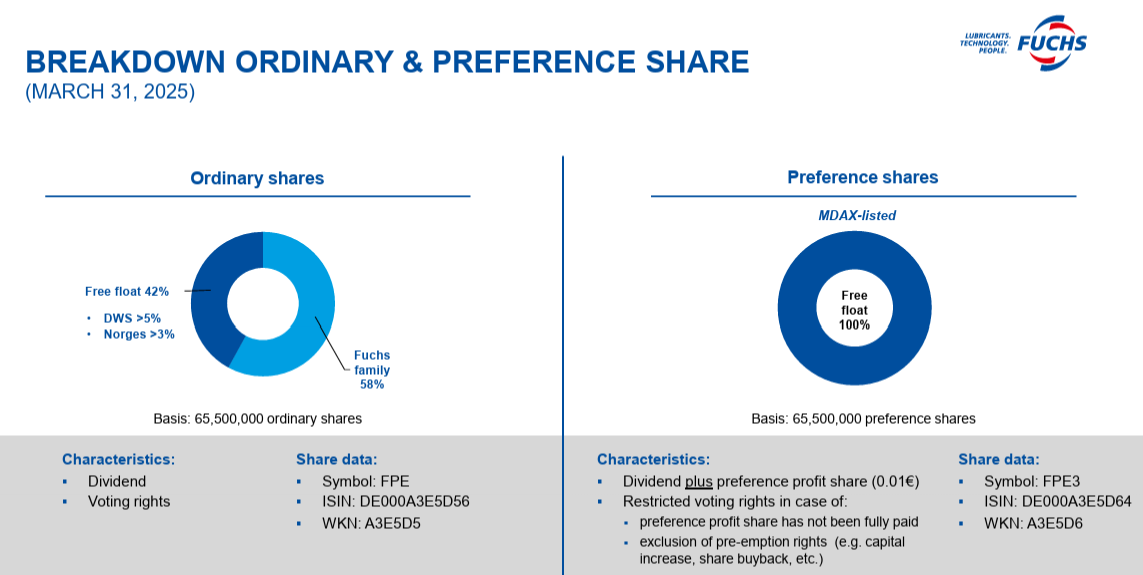

Management and Ownership Structure

A defining feature of FUCHS is its family-controlled ownership structure. The founding family retains majority voting rights through ordinary shares, while preference shares are fully free-float and listed, ensuring market liquidity alongside long-term control.

This structure aligns management incentives with long-term value creation and supports disciplined decision-making across cycles.

Source: FUCHS SE – Investor Presentation

The company is led by the third generation of the founding family, reinforcing a culture focused on continuity, operational excellence and prudent capital allocation rather than short-term expansion. Governance follows established German standards, and there is no evidence of excessive risk-taking or shareholder-unfriendly behavior.

Generally, this ownership and governance framework provides stability and strategic consistency, which is particularly valuable in an industrial business exposed to economic cycles.

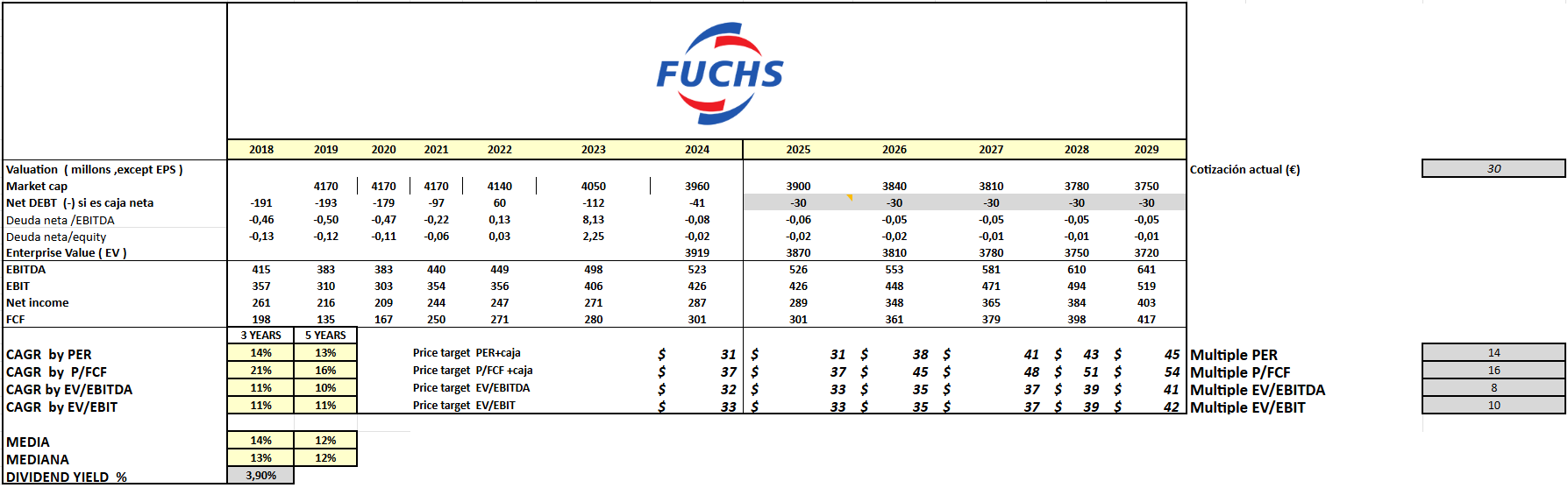

Valuation

As usual in order to assess the value of the analyzed company I do 3 different approaches: trading multiples, a simplified discounted cash-flow model, and a sensitivity analysis. Together, these three methods provide a balanced and ilustrative view of the company’s worth.

The goal is not to provide a precise target price, but to outline a reasonable valuation range grounded in the company’s fundamentals and reported financial performance.

Disclaimer: (The following is a conceptual valuation framework based on public historical data. It is an illustrative example and not an investment recommendation.)

Here we combine historical reported figures with forward projections based on the company’s own guidance and recent performance trends.

This valuation approach is based on historical company data combined with forward projections and peer multiples. Fuchs is compared with listed poultry and food processing peers using P/E, EV/EBITDA and EV/EBIT benchmarks. The model applies sector-average multiples to projected earnings, providing a relative valuation range grounded in comparable market pricing rather than standalone assumptions.

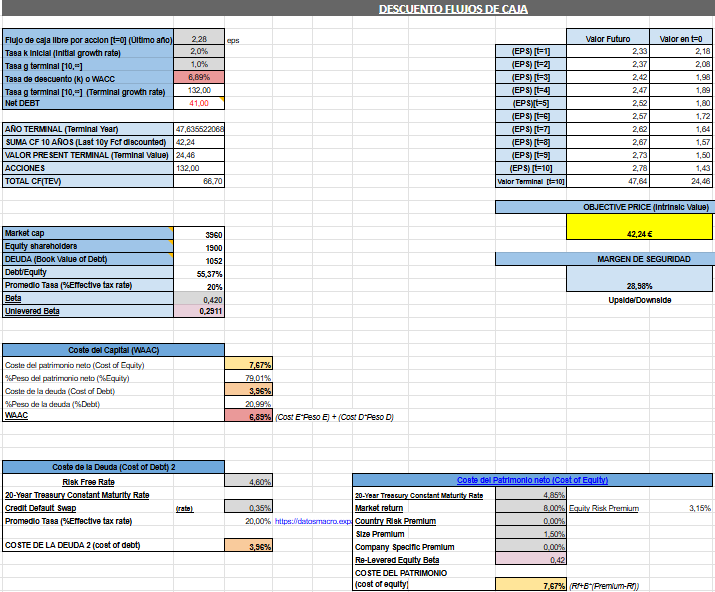

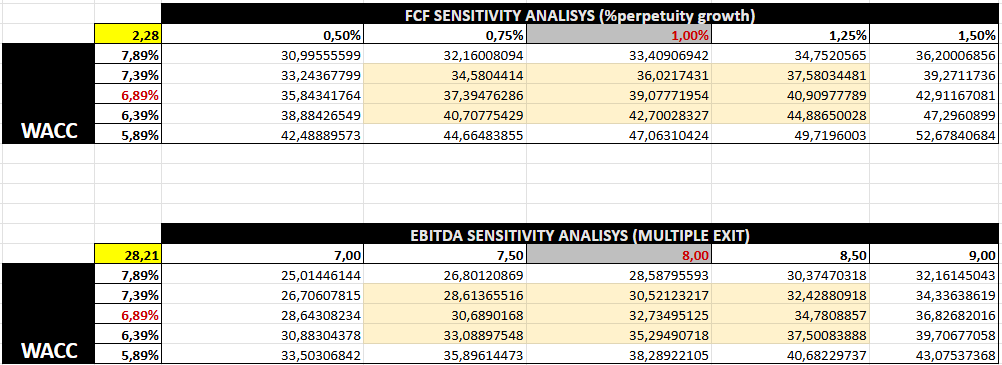

The DCF valuation is built on historical data and conservative growth assumptions. Applying a 6.89% WACC and modest terminal growth, the model yields an intrinsic value of 42,24€ per share.

Finally, this sensitivity analysis gives additional perspective on how valuation changes depending on key assumptions such as WACC and long-term growth.

Rather than relying on a single output, it provides a valuation range under different possible scenarios. This improves the robustness of the analysis and helps frame the investment case in terms of risk, upside and margin of safety.

CONCLUSION

Fuchs is best understood as a stable, family-run Industrial business operating in essential markets with predictable demand.

We should not see Fuchs as a ¨growth¨ company, but a defensive business with predictable cash generation and long-term compounding potential.

At reasonable valuation multiples, the market effectively prices Fuchs as a low-growth industrial, however, the market may be underestimating the value of its resilience, scale and demand from new megatrends and company strategic positioning.

Magno Investments Research

⚠️ DISCLAIMER | LEGAL ADVICE⚠️

Magno investments is not an entity authorised or supervised by any financial authority and does not provide investment services or regulated financial advice.

All material provided (articles, presentations, theses, ideas, opinions and analyses) are for informational and educational purposes only and does not constitute a recommendation to buy, sell or hold financial instruments, nor does it constitute personalised advice

Magno Investments Research are not responsible for the use made of this information or the veracity of its sources.

Magno Investments and/or its writer and contributors may hold, directly or indirectly, positions in the securities mentioned in the content. These positions may be changed at any time without prior notice.

Before investing in a real account, it is necessary to have the appropriate training or otherwise delegate this task to a professional duly authorized to do it. Magno Investments is not responsible for the use that members make of the information or for any losses arising from their investments.